Rising commodity prices: causes and implications

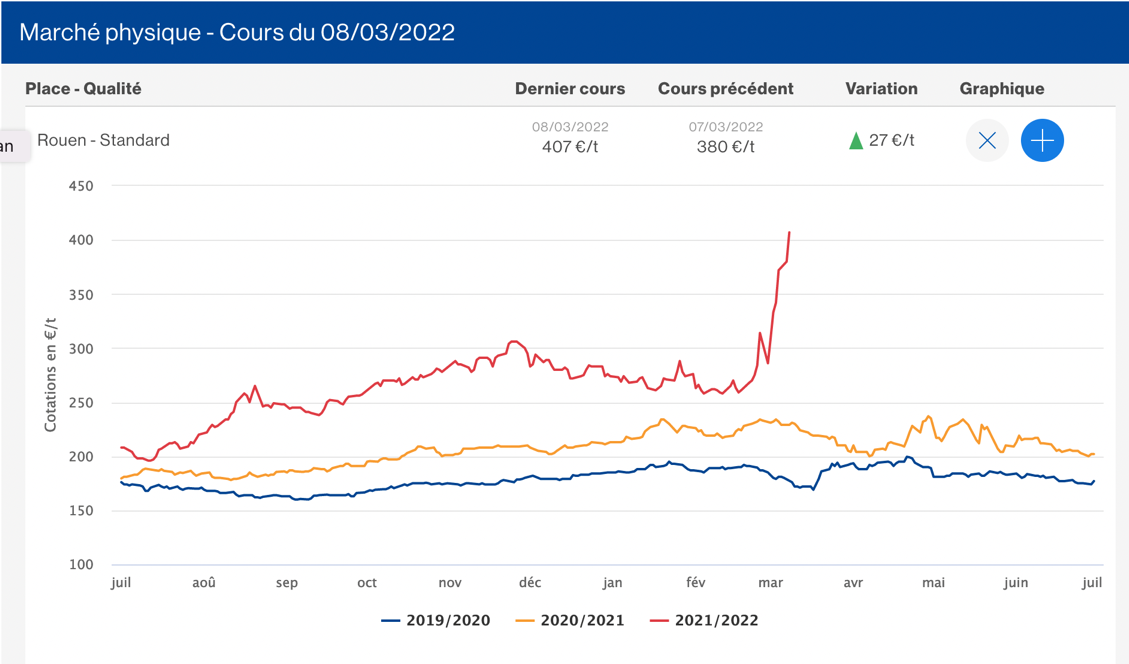

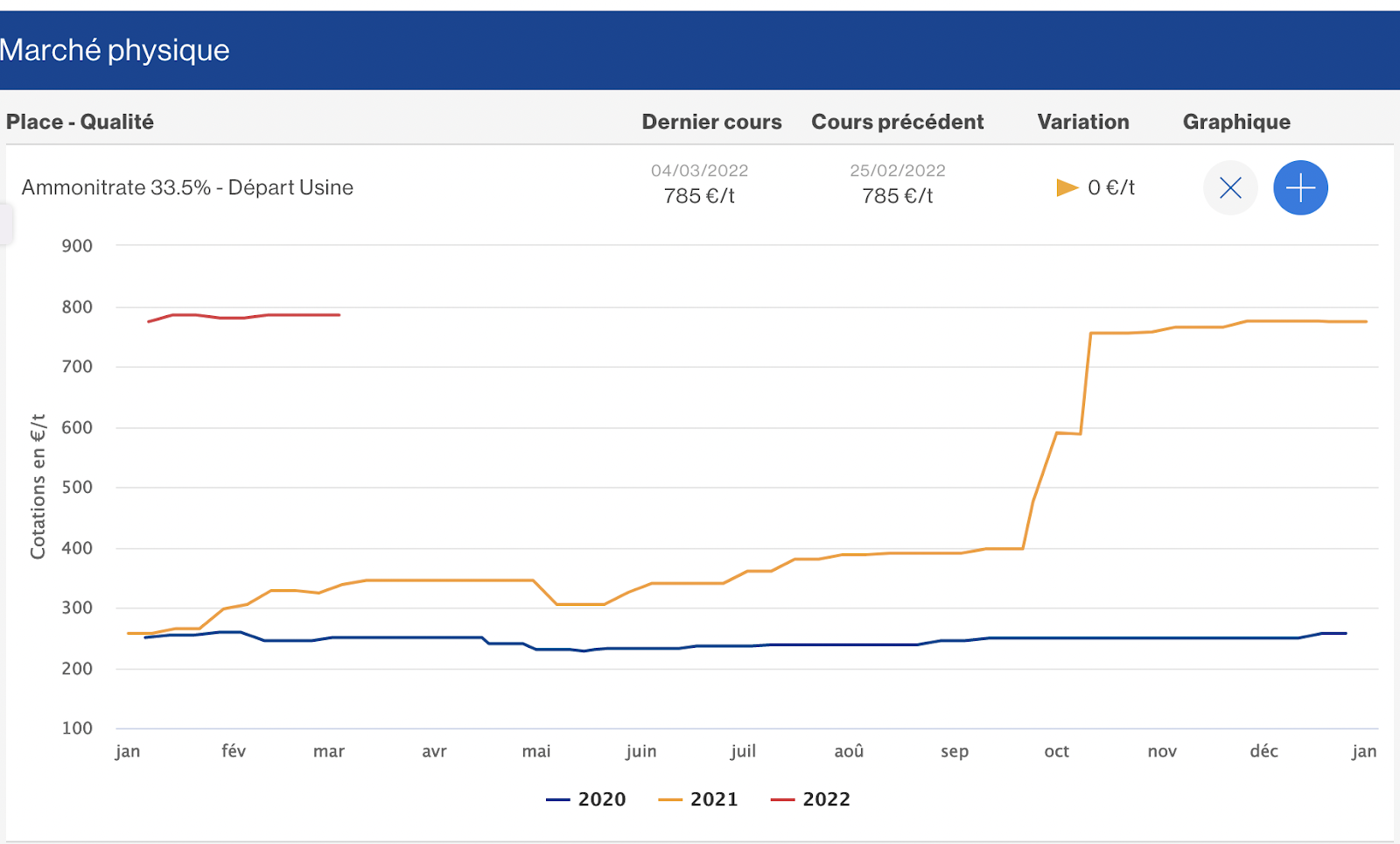

The current rise in agricultural commodity prices is linked to two factors. Firstly, the blockage of exports from the Black Sea is making it difficult for many importers to obtain supplies on the physical markets. On the futures markets, it is the fear of a shortage - should the conflict prevent the cultivation of maize and sunflower or the harvesting of wheat - that is fuelling an upward trend. This follows a steady rise in grain prices over the past six months, driven by the rising cost of gas and, in turn, nitrogen fertilisers (the price of which has risen more than threefold since January 2021). The conflict is thus exacerbating a trend that had already influenced fertiliser purchasing strategies and current planting. As a result, wheat prices on the futures markets are breaking records, at over €400/tonne (as of 8 March), above the prices reached during the 2007 food price crisis.

Figure 1: Wheat prices per tonne, 2019-2022

Figure 2: Ammonium nitrate price, reference nitrogen fertiliser, 2020-2022

To understand the implications of this price increase, it is necessary to distinguish between two dimensions of food security: the physical availability of food; and its economic accessibility. A distinction must also be made between time horizons.

In the short term, there is no direct challenge to physical availability: the crops blocked in Ukraine have not been destroyed, and the buyers who were to receive these deliveries have turned to other suppliers. The problem concerns economic accessibility: at 400 €/t of wheat for delivery in March, i.e. more than 2.5 times its 2020 price, further increased by additional logistics costs, the effects are colossal. They are felt by North African and the Middle Eastern countries, which are heavily dependent on imports (around 10% of their domestic cereal needs are imported- 1/5 of which comes from Ukraine). This price increase is also proving extremely difficult to manage for European livestock systems, which are increasingly dependent on imported feed. Indeed, these farms absorb 60% of cereals and nearly 70% of oilseed consumed in Europe in the form of concentrates, a large proportion of which is imported from world markets. In this respect, what is at stake - at least in the short term - is not Europe's "food sovereignty" - a term used today as a synonym for food self-sufficiency, whereas it was coined to designate the right of all citizens to define their own agricultural and food system. Rather, it is Europe's ability to maintain an intensive livestock industry that is competitive in the face of international competition and able to provide consumers with low-cost animal products.

What can and should Europe do about this situation?

In the short term (a few weeks), the priority is to mitigate the price increase for those countries most dependent on imports - in particular those countries where the Arab revolutions of 2011 were triggered by protests against rising food prices. The EU and its Member States can contribute in a number of ways. Firstly, they can increase their support to the food security support schemes managed by the World Food Programme, which currently amounts to almost €2bn/year (€465m/year for the Commission and €1.47bn/year for the Member States), drawing on the solidarity and emergency reserve provided for in the multi-annual financial framework (€1.2bn, of which 35% can be used for third countries). They can also increase bilateral aid to countries that will have to put in place emergency measures for their population (monetary or food transfers). And finally, they can support the countries concerned in releasing the strategic stocks that most of them have built up.

In the medium term, the stakes will vary depending on how the conflict develops. If the fighting continues to be confined to urban areas, maize and sunflower planting - due by mid-April - and wheat harvesting - at the end of June/beginning of July - could proceed without interruption. Prices will inevitably remain high - as long as Ukraine has not regained control of its stocks and gas prices are high - but the risks of physical supply disruption are low. Europe's role will be to continue to support the most import-dependent countries to avoid a period of high prices turning into a food disaster.

If, on the other hand, the conflict prevents the planting of maize and sunflower areas - i.e. a little over 11 Mha - or the harvesting of wheat - an additional 6.5 Mha - the physical availability of cereals and oilseeds will be directly affected. In the medium term, this could affect Ukraine itself - even if it is temporarily sheltered by its large stocks, linked to a very high export/production ratio (70% for cereals, 30% for oilseeds); but all the countries dependent on Ukraine (led by Egypt), which account for 8 to 10% of world exports of cereals and oilseeds, will be in difficulty.

The contribution of the Farm to Fork Strategy

Should we then, as some suggest, seek to produce more in Europe to compensate for this (potential) reduction in supply? Or even to gut the F2F strategy, which would be fundamentally 'unsuited' to the current challenges because it pays too much attention to environmental issues? Such an approach would be counterproductive in many ways. On the contrary, systemic change as supported by the F2F will be needed to respond to the challenges raised by this crisis and to progressively improve the EU's contribution to global food balances.

First, it should be remembered that the room for manoeuvre to produce more grain in Europe is limited. Some commentators have suggested using the "set-aside" areas, or areas of ecological interest, that the EU has (a little over 8.5 Mha today) to grow cereals. However, the areas currently available probably do not exceed 6 Mha (out of 100 Mha of arable land), and the potential yields are low, as these set-aside areas are on marginal lands. Additionally, these areas would need to be prepared by farmers, and the seed for maize, spring barley or sunflower (which is being sown now) would have to be available, which is not the case. Moreover, in the current state of cropping systems, growing more to produce more means using more mineral nitrogen, which is now massively imported from third countries (including Russia, Ukraine and Belarus, which account for nearly 20% of total nitrogen fertiliser exports) or produced in Europe with gas, the price of which is soaring. Finally, and probably most importantly, yields in Europe have been stagnating for many years in most Western European countries, and it is not environmental regulations that are limiting yields, but rather climate shocks, loss of pollinators, and soil degradation. Seeking to cultivate more, by mobilising more nitrogen, destroying what remains of ecological interest, or mobilising more water, will only further degrade the productive capacity of agrosystems - and make it close to impossible to increase expected yields.

As Europe cannot hope to produce more, it is only by reorganising its food system as a whole as the F2F is trying to do, that it will be able to increase its contribution to the world food balance, even with constant or even reduced production. This is what our recent work on the impact of an agro-ecological Europe on land use and global food security shows. At the heart of the more sustainable and resilient food system we describe are new ways of producing and consuming animal products. Because of its imports of soybeans and sunflowers to feed industrial livestock, the EU is now a net importer of calories: it depends on the rest of the world for 10% of its consumption. This is in a context where the consumption of animal proteins is almost double that required to cover our nutritional needs. A 40% reduction in the consumption of animal products, and a transition to low-fodder and self-sufficient livestock farming (i.e. fed on European grasslands and legumes), would thus make it possible: (1) to move the EU from being a net importer to a net exporter of calories; (2) to reduce our carbon footprint and contribute to restoring the biodiversity of European agrosystems; (3) to reduce our dependence on natural gas and fossil fuels for fertiliser production; (4) and finally to make room on our plates for essential - and under-consumed - foods such as fruit and vegetables.

Such a transition, outlined by the F2F strategy, requires financial and human support commensurate with the challenges. A gradual reduction in animal production fed on grain and oilcake would be an appropriate response to an emergency situation, while being part of a coherent agro-ecological and food project. The Netherlands has shown that such a policy is feasible, and it seems to us that it should be put on the table as an option. In financial terms, the costs of transitioning to a system with fewer grain-fed animals does not appear to be more expensive than supporting the import of synthetic inputs. The Farm to Fork Strategy presents opportunities to prevent future food crises, and should not be thrown out for unclear benefits.